Shopify Analysis 🛒🌐💸

Shopify Analysis 🛒🌐💸

Shopify's been one of the biggest gainers in my portfolio since I first bought it in 2017. But how has the underlying business performed since then and am I considering closing the position?

**Disclaimer: The information provided herein is for educational and informational purposes only and should not be construed as financial advice. This information is not intended to be a substitute for professional financial advice, analysis or guidance. Any actions taken based on the information provided are at the sole discretion and responsibility of the reader.**

The realm of e-commerce has undergone a huge transformation in the last decade, with online shopping gaining popularity. As a result, companies like Shopify (NYSE: SHOP), an e-commerce platform, have witnessed tremendous growth.

At first glance, and based purely on fundamentals, it seems questionable to be buying shares at present; they already trade at close to 10 times Shopify’s forward sales while the business itself is barely profitable.

But Shopify's stellar performance in the e-commerce market makes it a significant player, and its Q4 2022 earnings results mean the company warrants a more in-depth analysis.

What is Shopify?

Shopify is an e-commerce platform founded by Tobias Lütke and Scott Lake in 2006. It initially operated as an online store specializing in snowboarding equipment before pivoting to become a platform to connect buyers and sellers online. With a global presence spanning over 175 countries, Shopify supports roughly 5 million jobs and has contributed an impressive $444 billion to the global economy.

Shopify is a subscription-based software-as-a-service (SaaS) sales platform that regular people can use to create an online store. Think of Shopify as arming the eCommerce rebels (around 25% of all online stores are powered by Shopify), whereas Amazon trying to build an eCommerce empire.

Shopify’s Finances

In February, Shopify dropped its 2022 annual report packed with figures about the company's financial health and future.

Gross Merchandise Volume

Shopify has been thriving financially and has the figures to prove it. Their gross merchandise volume (GMV - the overall value of goods sold on their platform), grew 16% from the previous year and now stands at an impressive $197.2 billion.

Shopify's Revenue

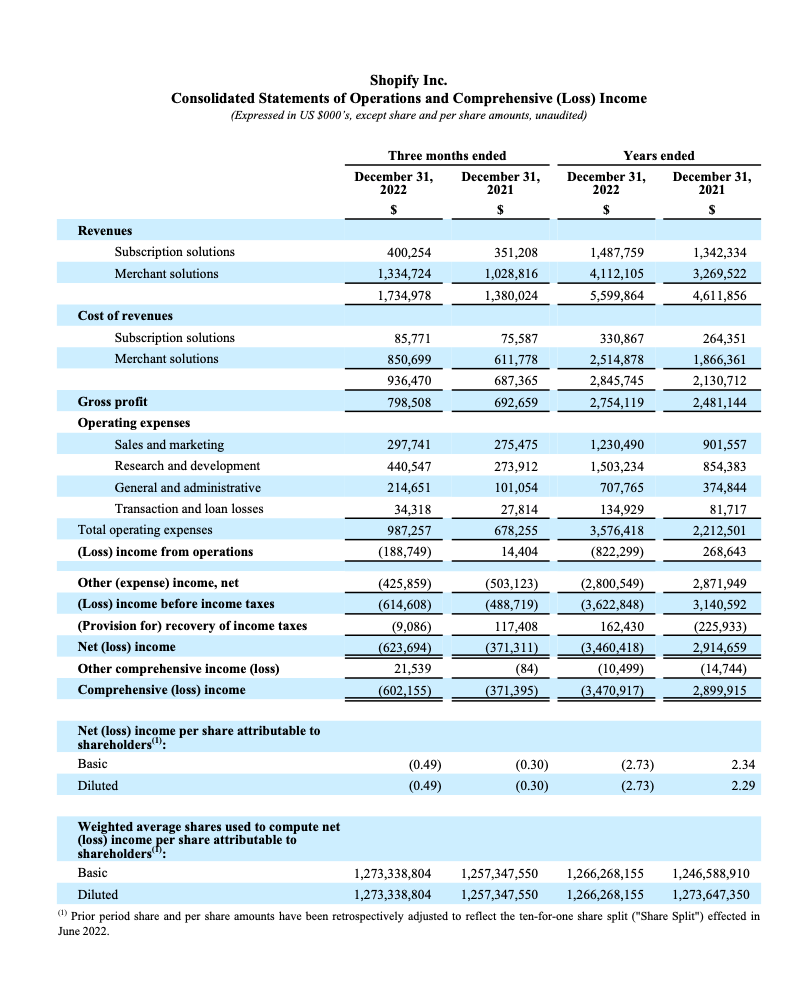

Shopify's revenue for 2022 surged 23% to $5.6 billion. Subscription revenue (revenue from store subscription plans) grew 11% to $1.5 billion and merchant solutions revenue (revenue from payment processing fees) grew 26% to $4.1 billion.

This is obviously far below the hyper-pandemic revenue growth of 57% in 2021 and 86% in 2020, but still respectable for a company that grew so much in the two years prior. The significant inflation in 2022 also no doubt impacted the company’s results.

Assets/Liabilities

Shopify’s 2022 annual report showed:

$10.76 billion in total assets ($6 billion short-term and $4.7 billion long-term).

$2.52 billion of total liabilities ($856 million short-term and $1.66 billion long-term).

The company has plenty of cash to spend on expansion and funding R&D.

Profit & Loss

Shopify’s gross profit grew in 2022 to $2.75 billion (for context, it was just $596 million in 2018) but this fell sharply to a loss of $3.56 billion once operating and other expenses were taken into account.

Thankfully, this is largely made up of unrealized losses on other equity holdings (affirm holdings and Global-E Online Ltd), rather than business-related expenses.

Operating expenses also accounted for a large part of the fall in net income, driven largely by an increase in R&D spending and sales and marketing.

The spend on sales and marketing is understandable given nearly 649 million people made a purchase from a Shopify store in 2022.

Nor does the spend on R&D give me any cause for concern. Last year Shopify introduced:

Shopify Collabs - A sales channel for merchants to find and collaborate with creators to promote products to new audiences.

Shopify Audiences - A marketing tool powered by an audience network and machine learning that helps merchants find high-intent buyers for their products.

POS Go - An all-in-one mobile POS device allowing merchants to accept payments on mobile.

LinkPop - A customizable link-in-bio tool that lets Shopify merchants sell products with shoppable links and gives users powerful analytics tools to see which contents and products captivate their followers.

With this many new releases, as well as the spending on improving the current products, it’s no wonder that the company’s R&D spend was high.

Shopify doesn’t expect to record GAAP profitability over the next few years; the company intends to remain focused on growth and vertical integration. Thankfully, it can afford to do this based on its healthy balance sheet mentioned above.

With the uncertain macroeconomic environment and slowing growth (albeit relative to the hyper-growth of e-commerce during the lockdowns) it’s unlikely that we’ll witness a quick and sustainable recovery to the $150+ levels we saw during the pandemic.

But product adoption, even though it’s the highest in its industry, is still growing fast. Shopify’s lack of GAAP profitability seems to be primarily down to its desire for fast growth which is understandable. However, it’s in a fast growing industry, is the leader in its niche, and has reported rapid revenue growth in the last 5 years; it did all this with a very healthy balance sheet.

The lack of forecast GAAP profitability is understandable and doesn’t give me cause for concern as an investor at the moment.

Risks

I’ve listed what I believe are a few of the main risks of investing in Shopify below.

Competition - Shopify operates in a highly competitive e-commerce market, and its merchants face competition from other e-commerce platforms like Amazon and Etsy. While Shopify has been able to differentiate itself by offering unique services to its merchants, there are also other competitors that provide services to online sellers such as WooCommerce or Wix.

Merchant Exposure - Shopify's revenue is also heavily dependent on small businesses. While this has been a strength in the past, it means that Shopify’s vulnerable to any economic downturns that could impact these businesses. If small businesses struggle, it would almost certainly impact Shopify's business too.

Reliability on Payment Processors - The company relies on third-party payment processors like PayPal and Stripe to process payments. While these companies are established and reliable, any issues with these payment processors could impact Shopify's ability to process transactions and hit the trust it’s built up with its merchants and customers.

Expansion Overseas - Shopify’s expanding into new markets around the world, which comes with additional risks including currency exchange rate fluctuations, compliance with local regulations, and adapting to local consumer preferences.

Future Prospects

Shopify's stock price is up 27% as of the start of April 2023.

Concerns about decelerating growth prompted the stock to drop following its Q4 2022 earnings report in the middle of February but Shopify's present value remains compelling in my opinion. Its current price-to-sales ratio is considerably lower than its mean over the past five years.

Despite a minor deceleration from 2022, Shopify's growth is projected to pick up pace in the coming year. Moreover, Shopify's projection for Q1 2023 is in line with the Street's expectations of a 20% surge. Analysts anticipate Shopify to wrap up 2023 with a 19% hike in revenue to $6.65 billion.

Investors should also consider the market in which Shopify operates, as the company is at the beginning of a multiyear growth curve. With a 10% share of the e-commerce market in the US alone, Shopify's multiple shipping solutions are well-positioned to ride growing e-commerce penetration in the US and worldwide.

The company estimates that it’s sitting on a total addressable market worth $160 billion, which means that it hasn't captured even 4% of its end-market opportunity based on its 2022 revenue. Statista also estimates that US retail e-commerce revenue is expected to grow from $905B in 2022 to over $1.7T by 2027.

Shopify is a stock that I believe is well-positioned for sustained expansion, and this makes it an attractive investment. Despite potential short-term fluctuations, the firm's outlook is promising, and it's in a favourable position to capitalize on the flourishing e-commerce sector.

Conclusion

Shopify is a powerful contender in the e-commerce industry, boasting a worldwide presence and a vast array of tools for businesses of all sizes. Despite fierce competition in the e-commerce arena, Shopify's extensive global user base, alluring merchant features, and expert team make it a sound investment choice in my opinion.

Its 2022 annual report shows financial stability, with substantial progress in several key areas. Though the company's gross profit margin took a hit due to contributions from lower-margin revenue streams, its impressive and steady growth in merchant cash advances and loans via the Shopify Capital program more than makes up for it.

If its revenue growth dropped to single digits, I’d seriously consider my position in the business. But until that happens I’m happy to remain invested.